December 12, 2025

Key takeaways

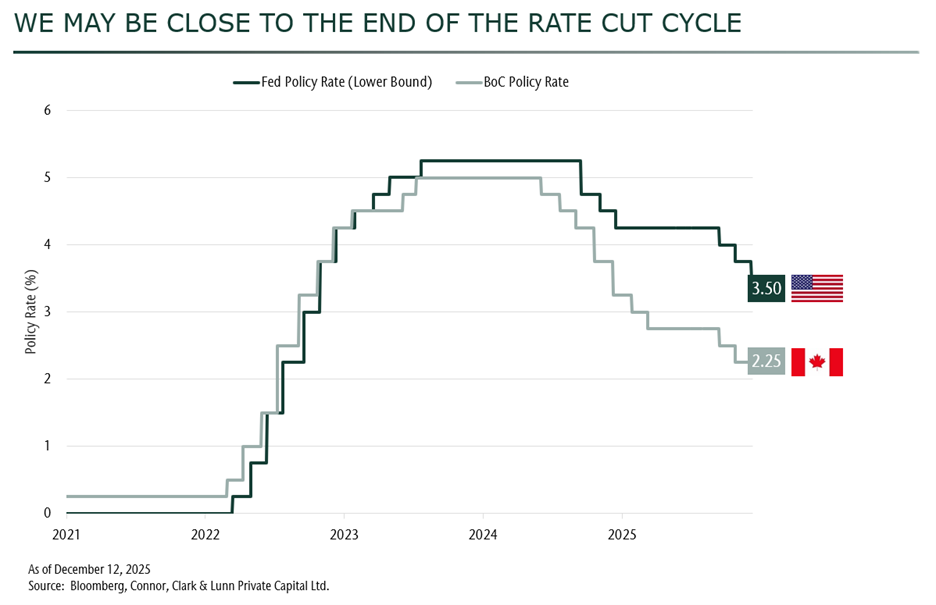

- The Federal Reserve cut rates to support the labour market, while the Bank of Canada held rates steady due to economic resilience.

- Future monetary policy is uncertain, and we see the risk of prolonged, above-target inflation complicating rate decisions.

- We could be approaching the end of the rate-cutting cycle that has supported equity and credit markets. We forecast positive but moderate returns going forward.

The United States (US) Federal Reserve (Fed) cut interest rates this week— a measured move aimed at supporting the labour market while moving policy toward a neutral stance. Fed Chair Powell emphasized that future decisions will be data-dependent,

rather than automatic.

The Bank of Canada (BoC) took a different tack, holding rates on the view that the Canadian economy remains resilient and closer to its 2% inflation target. Markets responded quickly: futures now price in two Fed cuts next year and a Canadian rate hike.

We view this reaction as too aggressive; our base case calls for a single Fed cut in 2026 and a BoC on hold.

Why this matters

Powell made clear that any further easing hinges on upcoming inflation and labour market data. The labour picture is particularly noisy. That uncertainty helps explain the Fed’s bias toward modest easing in an effort to guard jobs rather than keeping

policy tight.

However, we see a risk of higher inflation next year coming from government stimulus and tariffs. While we believe the effects on inflation are ultimately temporary, this could keep headline inflation well-above target for longer than markets assume,

complicating the Fed’s path.

How this plays for markets

Moderating inflation and cooling labour markets have created an economic environment supportive of equities and credit this year, as these conditions have justified rate cuts. The Fed’s latest rate cut preserves that constructive picture,

however, we believe that we will see fewer cuts going forward.

If this comes to pass, the upside for equities would be limited. The biggest threat is renewed inflation that prevents further easing or forces a policy reversal. The latter scenario could prompt a rapid repricing of short-term rates and hurt both bonds

and stocks. Conversely, a material slowdown in growth would justify additional easing and potentially boost markets.

What we're watching

We’re focused on inflation and signs of tariff pass-through, and weekly jobless claims and monthly payrolls (including revisions), as well as Fed language and internal dissents, and BoC commentary. This data will determine whether markets’

aggressive expectations for easing are rewarded — or corrected.

The bottom line

We think the balance of risks supports fewer cuts. We remain positioned to capture further upside in equities and credit while preserving flexibility and protection against a rise in inflation — a risk we believe markets are underestimating.