November 28, 2025

Key takeaways

- US consumer spending remains resilient, but confidence is falling due to persistent inflation and higher prices.

- Earnings are supported by high income spenders and AI investment.

- The Fed is now more likely to cut rates at their December meeting and stocks have rallied.

Black Friday is a good moment to take stock of the consumer. In the United States (US), spending remains resilient. Incomes continue to grow—especially for higher-income households—and we expect this support to carry into next year.

A “low-hire, low-fire” labour market

While the labour market remains solid, it is cooling. Companies aren’t hiring aggressively, but they’re not laying people off either. This dynamic should keep income growth steady enough to support modest consumption into 2026.

However, the jobs market could weaken further. If it does, the Federal Reserve (Fed) is likely to respond with more rate cuts—providing support to employment and income growth.

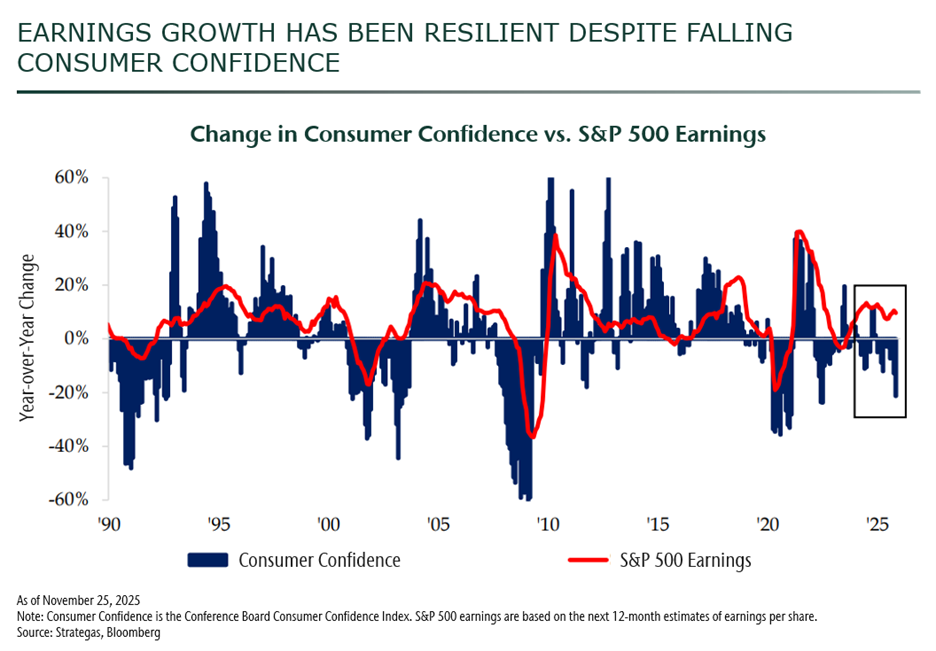

While spending is resilient, confidence is waning

Despite solid incomes, consumer confidence is falling. The culprit is clear: prices are much higher than just a few years ago, and inflation—while moderating—still bites. This pessimism could eventually weigh on spending and corporate earnings.

Historically, consumer confidence and earnings growth move together. Today, they are diverging and we think that this gap could persist for two reasons:

- Lower-income households are driving weak confidence. That being said, they now represent a smaller share of total spending. Higher-income consumers, who remain in good shape, are carrying overall consumption.

- Market earnings are not solely reliant on the consumer. Artificial Intelligence (AI)-driven investment continues to deliver strong earnings for large technology companies. This strength is likely to extend into 2026.

The Fed is now expected to cut in December

The Fed is navigating the tension between cooling inflation and a softening labour market. Expectations for a December cut have swung sharply—from above 80% in September, to below 50% two weeks ago, and now back up to roughly 80%.

What changed? The government shutdown disrupted economic data releases, leaving investors with an incomplete picture of the economy. With key labour and inflation numbers delayed past the next Fed meeting, markets have leaned more heavily on survey data—which

has deteriorated.

The Fed’s decision will have far-reaching implications for the market.

- If the Fed holds rates steady, markets will likely be disappointed given current expectations.

- If the Fed cuts rates, policy will remain accommodative at a time when early-2026 fiscal stimulus may lift growth. This combination could set the stage for renewed inflation pressure—a classic challenge for policymakers.

We think the macro picture is improving. However, with markets priced for a steady stream of good news, we’re mindful of the risks that lie ahead should this fail to materialize.