January 20, 2026

.png?sfvrsn=dc17a93a_3)

While many people have an idea of how much they would like to spend each year during retirement, they feel uncertain about whether their portfolio can sustain it and wrestle with other spending priorities. Can I help my children with a down payment on their first home? Can I make a sizeable donation to charity? Will doing so compromise my lifestyle in retirement? Understanding the difference between core and excess capital can guide you in answering such questions.

What is core capital?

Core capital is the wealth an investor needs now to fund future retirement expenses with a high degree of confidence (typically with a 90% probability). Core capital represents the essential assets required to sustain your lifestyle over a

chosen time horizon, such as retirement.

What is excess capital?

For those with wealth beyond their means, excess capital is the amount currently available that is not required to support key future spending goals. Excess capital serves as a buffer, offering flexibility for discretionary purposes such as large additional purchases, philanthropy, and legacy planning.

How to calculate core and excess capital

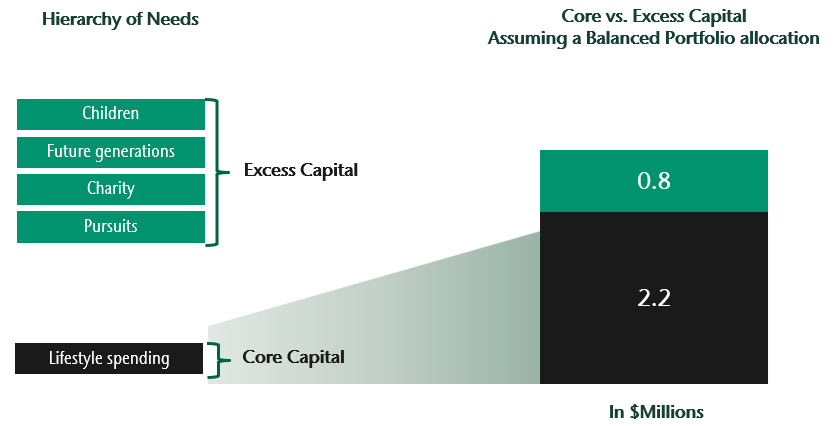

Consider a 65-year-old retiree in British Columbia, who expects to live for another 25 years. The retiree has $3 million invested in a personal taxable account (balanced investment strategy). Going forward, the retiree would like to spend $100,000 annually after-tax, grown for inflation. Assuming the portfolio is their only source of income, a custom CC&L Private Capital analysis suggests that they would require $2.2 million invested today.

A CC&L Private Capital balanced investment portfolio is typically comprised of 32% fixed income, 13% hedge strategies, and 55% equities (long-term target weights). With $2.2 million invested in such a strategy, our forecasts suggest with a reasonably high degree of confidence that the retiree will not run out of capital in their lifetime (by age 90). Therefore, we consider the remaining $800,000 (of their $3 million in investment assets) to be excess

capital.

Core vs. Excess Capital ($ millions)1

Determining your essential and discretionary retirement funds

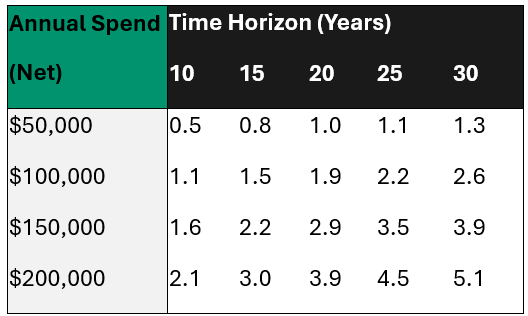

Your anticipated spending level and time horizon are amongst the key variables in calculating core and excess capital. The following table illustrates core capital requirements for various spending rates and time frames using CC&L Private Capital forecasts and a balanced asset mix.

While this information can be a helpful guideline, it does not replace a custom analysis that considers changes in asset mix, account types, outside income sources, and unique tax situations.

Core Capital Requirements ($Millions)2

Core and excess capital values are based on calculations and forecasts of future investment performance that can never be 100% certain. However, at CC&L Private Capital, we can estimate clients' core and excess capital with a high degree of confidence, such that the core capital amount will be able to sustain clients' planned spending over the given time horizon —even if financial markets perform poorly.

We simulate 1,000 potential investment return scenarios, looking for a core capital amount that provides adequate resources in at least 900 of those scenarios. This gives us the high degree of confidence necessary to enable our clients to feel confident in their chosen investment strategy. Those conservative clients who wish for an even higher degree of confidence are accommodated by utilizing a higher level of core capital.

Factors influencing core and excess capital calculations for retirement planning

Many high-net-worth individuals receive rental income, part-time consulting fees, work pensions, and / or government benefits during retirement. These incomes can offset annual spending needs and therefore reduce core capital.

For instance, suppose the 65-year-old retiree in our example receives $20,000 annually in pre-tax pension benefits (indexed for inflation). In this case, their core capital would decrease from $2.2 million to $1.9 million as the required draw from their investments is smaller.

Additionally, tax rules and return expectations vary across asset classes and account types. RRSP withdrawals, for example, are subject to withholding tax, unlike distributions from other account types. Therefore, retirees with a high proportion of retirement savings in registered accounts may have higher core capital requirements due to larger tax obligations.

Conclusion

Understanding your core and excess capital helps you determine the investment strategy most appropriate for you and helps you to make better-informed investment decisions. Core capital calculations reveal what you need for future

expenses; while identifying excess capital enables you to confidently spend or bequeath funds today. Fill in the form below to speak to one of our Wealth Advisors and learn more about your core and excess capital.