July 07, 2021

Markets overview

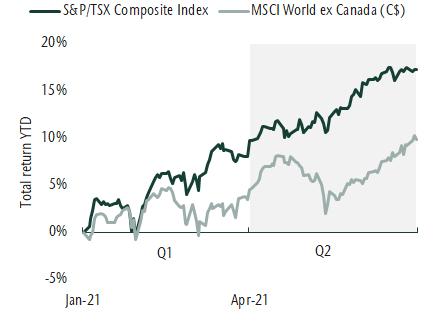

This quarter we saw the economic recovery continue to gather pace. Support for the recovery has come from easing restrictions and accommodative policy. More recently, countries have committed to expanding their spending programs to fight the remaining negative effects of the pandemic while improving longer-term growth prospects. Together this forms a positive backdrop for equities and we have seen companies significantly outpace earnings expectations. This quarter the S&P/TSX Composite Index was up 8.5% and the MSCI World ex Canada (C$) advanced 6.2%. Year to date this brings these market returns to 17.3% and 9.9%, respectively. Stronger performance from the S&P/TSX Composite reflects a strong Canadian dollar and a higher weight in the index to top performing cyclical sectors like energy and financials. Regardless, both Canadian and global results have been very strong.

Equity markets reach new highs

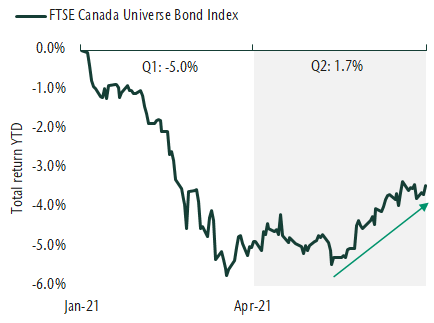

Bond returns have shown recent improvement after declining earlier in the year. This quarter the market has largely looked through a sharp increase in inflation which has been fueled by the robust economic recovery. Bond yields have declined modestly and prices have moved higher. The result was an increase of 1.7% for the FTSE Canada Universe Bond Index this quarter. The largest contributors to performance have come from provincial and corporate bonds.

Bonds begin recovery from Q1 decline

Portfolio strategy

Our view is that we are in the midst of a strong economic recovery supported by pent up demand, accommodative policy and record levels of fiscal stimulus. This is a market-friendly backdrop and portfolios have been positioned to benefit from the recovery. We have been tactically overweight equities. As equity market performance has been strong, we have taken profits and rebalanced to maintain our desired exposure. Within equities, we have an overweight to small-cap stocks and maintain an allocation to value stocks. This quarter we also increased our emerging markets position. Within bonds, we have been overweight high yield, which is attractive in the early stages of a market cycle. This asset mix positioning has served us well and remains attractive in the current environment.

Our portfolio management teams generally continue to favour more cyclical companies that are levered to the economic recovery. These stocks have done well and in select cases we have reduced our exposure. This is because while the economic recovery has been strong, results have begun to moderate. At the same time, inflation has been higher than expected. While we don’t believe inflation levels will be disruptive in the long term, current conditions may lead to market volatility. Within fixed income, similar to equity portfolios, we remain overweight companies that are benefiting from the reopening of the economy.

From the desk of Jeff Guise, Managing Director, Chief Investment Officer, CC&L Private Capital.

This post is for information only and is not intended as investment advice. The views expressed are those of the author at the time of publication and are subject to change at any time.