March 08, 2021

In typical fashion, markets have reflected opposing sentiments – uncertainty and optimism. On the one hand, the worry associated with the pandemic and on the other, optimism fueled by a resurgence in activity and strong government support. Our portfolio management and asset allocation teams have been busy, first and foremost, protecting capital during the market decline and then shifting positioning to benefit from the recovery. As we look forward here are some areas of opportunity we see as we manage client capital through a challenging time.

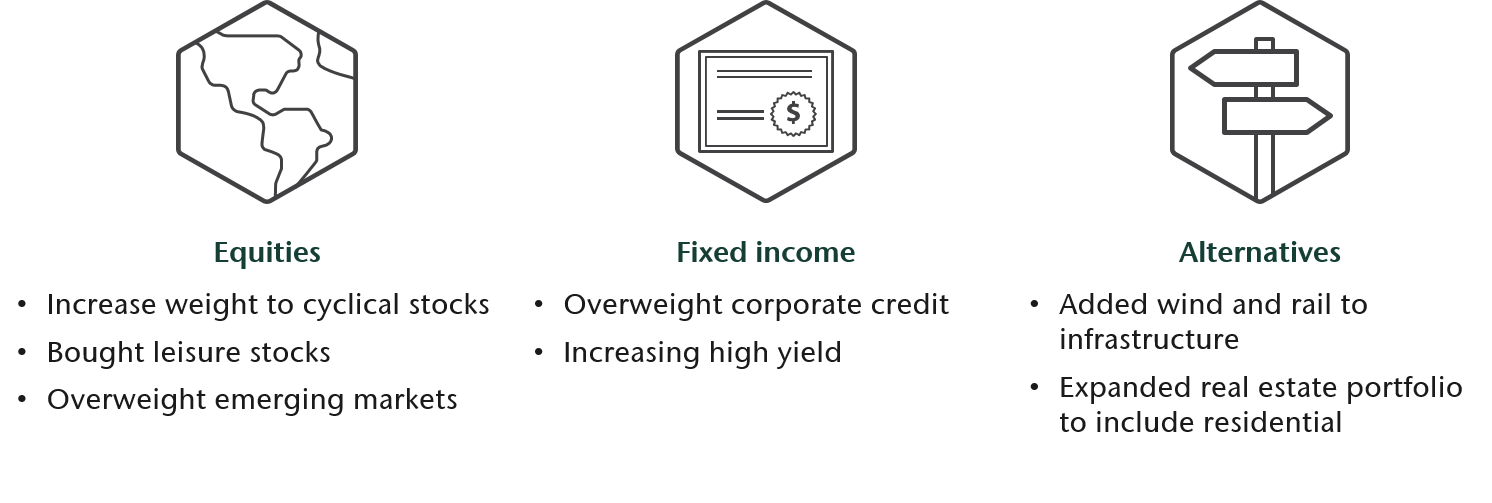

Revisiting equity exposure for a changing environment

Some investors might conclude that mega-cap stocks in Canada and US are the only place to be. Companies like Shopify, Facebook, Amazon, Microsoft, Apple and Google had very strong returns and our portfolios benefited from owning them. However, the recovery in stocks has broadened beyond these names. For example, in late 2020 we saw a resurgence in companies that were hurt most from lockdowns. With new vaccines these companies got a new lease on life. Throughout the year our teams took profits by selling some of the mega-cap stocks and buying companies likely to benefit from a post-vaccine world. This includes buying leaders in the travel and leisure industry. This may be hard to imagine at this point of COVID fatigue, but remember markets are always looking forward.

Late last year investors also began to favour areas that are more cyclical like value stocks, small-cap and emerging markets. These areas of the market were laggards earlier last year and have now risen above the pack. We were positioned for this shift in leadership by having a strategic allocation to value stocks and tactically buying small-cap and emerging earlier in the year. Today we are overweight equities in client portfolios with a bias to global small-cap companies. We believe we will benefit from a strong earnings recovery as more businesses reopen and stimulus remains a strong tailwind. We have also continued to increase our weight in emerging markets companies and recently launched a frontier equities strategy. As we look longer-term we believe these asset classes will be important sources of return in portfolios.

Bond investing in the wake of a pandemic

Our positioning in bond portfolios also reflects that the worst appears to be over. Yet we are not in the clear and safety is important in a bond portfolio. The challenge, however, is that the tradeoff for safety is low yields. Current yields remain lower than they were before the pandemic and central banks are inclined to keep them low. Our bond portfolios are positioned to improve yield by investing in high quality corporate and provincial bonds. We also believe that government stimulus will result in rising inflation expectations. This has led us to own real return bonds which will benefit from this trend. Finally, we have positioned the portfolio to benefit if the recovery stalls and bond yields fall. This is a prudent offset to other positioning and helps protect capital should the economic recovery falter.

As we look to strike a balance between safety and income, we have also been adding to high yield bonds that carry a much higher yield. The focus here is on strong credit research to avoid companies that may not be resilient if economic recovery stalls.

Fertile ground for alternatives

Private market alternatives have been an attractive addition to portfolios for some time. These assets can be generally characterized as having strong returns, coming mostly from income and relatively low volatility. This combined with added diversification makes private market alternatives appealing on a long-term basis. The tradeoff for accessing these characteristics is reduced liquidity and the time it takes to deploy capital into new assets. Recently, however, we have been able to put more client assets to work in these strategies. Within our infrastructure portfolio we completed the purchase of four operating wind assets and one construction-stage solar project in the US. These assets have strong expected returns and benefit from fixed price contracts for the energy produced. Not to mention this now brings our renewable power generation to 1.4 gigawatts, enough energy to power more than 320,000 homes.

Within our direct real estate portfolio we have completed our first purchase in the residential apartment sector. Historically residential has generated more stable returns and income compared to other property types like retail and office. We expect our allocation to this property type will increase.

Our positioning

The bumpy road to long-term performance

Building wealth for the future requires discipline, thorough research and a process for managing risk. The opportunities that are most attractive today are assets that can benefit the most from the economic recovery. Yet we also need to recognize that the road to recovery from here will be bumpier than what we’ve experienced so far. To manage this risk we continue to be broadly diversified while tactically tilting the portfolio to the areas of the market with the greatest opportunity.